)

)

)

Business philosophy15 Sep 2025

Stephen J. Squeri: American Express Veteran Chairman and CEO

Stephen Squeri has spent over four decades at American Express, rising through the ranks to lead one of the world's most recognized brands.

When you think of a credit card brand, you more than likely think of American Express. What began in 1850 as a parcel delivery business evolved into financial services, and eventually the credit cards that define it today. Today, the company's payment network, affluent customer base, and reputation all reinforce one another, creating a foundation that continues to grow stronger over time. Join us as we explore how history, brand, and structure combine to make American Express a business unlike any other.

If you've ever studied Warren Buffett and Berkshire Hathaway, chances are you've come across American Express more than once. He first bought shares of American Express in 1964 and exited the position four years later. Three decades later, between 1991 and 1995, Berkshire Hathaway built up a sizeable stake in the company, eventually owning 10%.

The position has sat untouched since then, and its decision to back Amex with capital during the 2008 financial crisis, along with years of stock buybacks, has lifted the firm's ownership to a little over 20%. The returns for Buffett and everyone else who held the stock throughout the decades have been outstanding:

What makes the American Express story so compelling in the context of Warren Buffett is not just the numbers, but the way it reflects the core ideas of his philosophy. American Express is a fantastic business and has several durable, interconnected competitive advantages that combine to form a powerful moat.

Buffett has not been shy about praising Amex for these qualities, and we promise to discuss them in depth in due time. But to understand the business and how the brand has become as strong as it is, we'll begin with its history. Let's head to Buffalo.

The American Express story begins on a cold and bitter day in March 1850. Three seasoned entrepreneurs, Henry Wells, William G. Fargo, and John Butterfield, met in Buffalo, New York, to finalize an agreement and merge their companies. The trio all owned and operated separate express companies with the same focus: transporting parcels, valuables, and financial documents.

Although the express industry was still in its early days, it was facing rapid growth. At the time, the U.S. Postal Service would not handle any package larger than a letter, which created a market for privately owned express delivery companies.

Wells, Fargo, and Butterfield's early-mover advantage had made them not only pioneers but also central players, with combined routes spanning from New York City to the Midwest. The merger created a joint-stock company that therefore came to dominate express shipping in the Eastern United States: American Express.

From the outset, Amex (as it's often referred to today) built a reputation for speed and trust, with banks quickly becoming its biggest customers. Almost instantly, it became apparent that shipping stock certificates, currency, and the contents of safety deposit boxes safely was far more profitable than hauling ordinary freight. Just like that, American Express had found its niche.

The U.S. was still a relatively young country, and like many other times throughout its history, it was evolving. Following the Mexican-American War, the U.S. acquired vast swathes of land, Oregon had just been recognized as a territory, and in 1848, gold was discovered in California. The country was clearly expanding, and as a result, commerce and the economy grew with it. Luckily for Wells, Fargo, and Butterfield, the merger had created a company able to tap into that demand.

As you read these opening paragraphs, you probably did a double-take when you saw the names Wells and Fargo. During the California Gold Rush, Henry Wells and William G. Fargo urged American Express to extend its service to the booming West Coast, but the board refused.

Undeterred, the pair struck out on their own in 1852, founding Wells Fargo & Company as a separate express and (eventually) banking enterprise focused on California and the Western frontier. This move essentially divided the market, with Wells Fargo dominating express service in the expanding West frontier, and American Express continuing to thrive in the East.

Get curated quality company deep dives every other week.

Amex grew explosively alongside the nation. By the end of the Civil War in 1865, it operated over 900 offices across 10 states and ran a network of stagecoaches and rail express routes nearly 10,000 miles long. But the success bred competition, and soon, a challenger had emerged. In 1866, the Merchants Union Express was founded and immediately launched a fierce rate war. For two years, they ruthlessly undercut one another, slowly but surely leading both to the brink of bankruptcy.

Unable to drive each other out of business and under the threat of mutual ruin, the two companies agreed to merge in 1868. Under William Fargo's leadership, the combined company was named American Merchants Union Express. After the consolidation was complete and the dust had settled, the name was reverted to American Express Company.

Throughout the remainder of the 1870s, American Express continued to grow its business with its stagecoach messengers and couriers connecting more and more parts of the country. William's younger brother, James C. Fargo, became President in 1881, and under his leadership, Amex launched a series of financial services that would completely redefine the business. The first of these was the American Express Money Order.

However, offering money orders wasn't an innovation from within American Express. The U.S. Post Office introduced them in 1864 as a safer alternative for sending payments at a time when mailing money was incredibly risky. For a small fee, anyone could purchase a postal money order, essentially a prepaid payment certificate, mail it to a payee, who could redeem it for cash at a post office.

Seeing the opportunity, and with an already existing and highly effective delivery network, James C. Fargo introduced American Express' own version in 1882. The service worked in virtually the same way as the government's version, but with some crucial new features.

American Express' version was designed with improved anti-tampering features, creating a safer instrument that was more difficult to forge or alter (a never-ending issue with the government's version). The process was similar to the aforementioned procedure, but with an Amex office as the intermediary. Instead of mailing cash to Aunt Pamela in Indiana, you could make a money order from your local Amex New York office and have her cash it in Indianapolis without much fuss.

It was an instant success, and within twelve months of launch, American Express had already issued over a quarter of a million money orders. The company generated revenue partly from the small service fees that it charged, but also from interest earned on money orders not yet cashed by the recipient. But more importantly for our story, the money order business was the start of a fundamental transformation for American Express from a delivery company to what it is today.

The inspiration for American Express' next service came to James Fargo while traveling in Europe, and facing the frustrating reality of international finance in the late 19th century. In those days, an American abroad would typically carry letters of credit from their bank, which (for the most part) would be honored by major European banks.

Accessing funds in a place like London or Paris would typically be relatively smooth and go off without any major problems. But walk into a local bank branch somewhere on the Amalfi coast, and cashing your letters of credit could be time-consuming or impossible due to wait times, language issues, wildly inaccurate exchange rates, and everything in between.

Fargo, of course, thought it was absolutely ridiculous. Here he was, the head of a major financial institution, yet still stuck waiting for cash on his European travels. Luckily, he was in a position to improve the situation.

Upon his return home, he immediately pushed for American Express to create a better solution. In 1891, the company introduced what would quickly become the preferred means for travelers to carry money: the American Express Traveler's Cheque. These were prepaid cheques available in various denominations that could easily be cashed abroad, with American Express guaranteeing the payment.

The product became a huge source of revenue in no time. Similar to the money orders, the traveler cheques generated revenue from fees, as well as the float sitting on American Express' balance sheet, earning interest. By the early 1900s, the company was generating over $6 million in revenue from its traveler's cheques annually, roughly $160 million in today's terms.

Just like with the money orders, the travelers' cheques served a dual purpose for American Express. Besides simply being an additional service, it built the company's brand and turned it into a household name among tourists and business travelers.

With the growing use of its traveler's cheques across Europe, the company expanded its physical reach beyond U.S. shores. In 1895, it opened its first European office in Paris, then branches in London and Berlin. As the 1900s began, the company was present on five continents, serving everything from leisure travelers in Europe and officials on business in Asia to millions of immigrants in America using money orders to send funds back home.

By the onset of the First World War, American Express was a financial services provider first, and a delivery company second.

The murder of Archduke Franz Ferdinand and his wife Sophie in 1914 lit the fuse of a Europe already primed for war. Like all companies with a presence on the continent, American Express suddenly faced a stark new challenge: operating in wartime. Thousands and thousands of American tourists, workers, and journalists were stranded in Europe, with many of them suddenly unable to access funds as local banks stopped honoring foreign letters of credit.

American Express, however, continued to cash travelers' cheques, providing funds to organize travel for Americans in a Europe that was being engulfed by war. Together with several U.S. banks, American Express also shipped millions of dollars worth of gold to Europe, helping to restore much-needed liquidity to local bank branches.

During the war, the company also became deeply involved in humanitarian operations and support of POWs. At the request of the British government, American Express offices in Europe helped deliver a range of items to Allied soldiers, including money, relief parcels, letters, and food.

While the company's work during WWI is commendable in its own right, it also served a secondary purpose that can't be ignored: it helped to cement American Express' reputation as a trustworthy company. Even as entire societies pivoted to support the war effort, it ensured that its cheques could be cashed.

Finally, as the guns of Europe fell silent and the major powers met in Versailles to sign the documents that would provide the continent with a much-awaited peace, the U.S. government threw a curveball. As part of its wartime control of the railroads, Washington consolidated the nation's express companies into a single entity: American Railway Express. Overnight, American Express' delivery operations were absorbed, never to return.

Forced (in hindsight, freed might actually be a better word) in 1918 to shed its delivery business, American Express went all-in on serving the ever-growing travel industry. However, the groundwork for this pivot had already been laid in the years prior, as the company had expanded its foreign remittance and banking operations and officially launched a travel department in 1915. What had originally been side ventures now became the core focus.

American Express continued to offer cheques and provide currency exchange, but it also acted as a travel agent, booking passage on steamships and trains, and even holding mail for traveling customers at its Amex offices. If you were an American far away from home in need of cash, a ticket to your next destination, or basically anything else, you'd search out a local American Express branch.

By the 1920s and 1930s, the company had established an international banking subsidiary and was marketing travelers' insurance, savings products, and other services. Leveraging the offers it had built during the previous decades, its new services met customers who already trusted the Amex brand. Even back then, the company was well aware that trust was its most valuable asset.

The interwar years continued to reinforce American Express' image as a trusted name in financial services, with the company steadily broadening its scope and deepening its role in the industry. Still, the defining product of its modern era would not arrive until decades later.

By the 1950s, a new financial product was rolling out to customers: the charge card, a predecessor to modern credit cards. The concept of a general-purpose charge card had emerged with Diners Club in 1950, and American Express, given its customer base and global merchant connections, saw an opportunity.

In 1958, it introduced its own version, which would change the company forever. The original cards were made of purple paperboard, and unlike a revolving credit card, cardholders had to pay off their balance in full each month. Initially targeting traveling businessmen and affluent consumers, the card allowed payment for things like flights, hotels, and restaurants, without the need to carry large amounts of cash.

By launch day, American Express had already placed 250,000 cards in the hands of customers, while securing over 17,000 merchants to accept them. If it sounds like an absolutely astonishing rollout, that's because it's precisely what it was. But it was only made possible by the company's already existing network, and like always, its credibility.

While American Express entered the 1960s with strong momentum in its card and travel businesses, it soon faced one of the most severe challenges in its history. In 1963, the company became embroiled in the infamous Salad Oil Scandal.

The full story of the scandal is complex and unusual, and well worth digging into if salad oil-based deception and financial fraud sound interesting. To keep it brief: an Amex warehousing subsidiary had unwittingly guaranteed fraudulent inventories of $150 million in vegetable oil used as collateral by a client to secure loans. However, what had been claimed to be oil tanks filled to the rim was in fact seawater topped with a thin layer of vegetable oil to disguise the fraud. When the scheme came to light, American Express' stock price was cut in half virtually overnight.

Ultimately, under the leadership of CEO Howard L. Clark, the company absorbed the losses, honoring all obligations and making affected lenders whole to uphold its reputation. Naturally, it was a staggering blow at the time, but it was rooted in a simple principle: trust in the brand came before everything else.

This is also where Warren Buffett enters our story. On the back of the scandal, he began conducting extensive due diligence, talking to bank tellers and officers, credit card users, hotel employees, restaurant workers, and anyone else who could offer insights into whether usage had fallen off. It proved it hadn't. Buffett concluded that the trust, integrity, and customer satisfaction with the brand were worth more than the short-term (and severe) cost of the bailout.

Buffett bet big. In 1964, he purchased 5% of the company's shares for $13 million, committing over 40% of his investment partnership's assets. Just as would be the case so many times in the decades to come, the Oracle of Omaha's judgment proved prescient. American Express emerged from the scandal bruised but, in due time, stronger. Buffett exited the position in 1968, selling his shares for $33 million.

While a return of 150% over four years is impressive by any standard, he has often expressed regret that he exited the position too early.

Through the mid-1960s and 1970s, American Express steadily grew its card business, pioneered new services, and launched highly successful ad campaigns. Two of the most notable additions to its business were the introduction of the Gold Card in 1966 and the Corporate Card in 1967, designed for business expense accounts. These offerings helped segment Amex's market toward premium customers, adding to the image of prestige and exclusivity. At the same time, the company aggressively expanded its merchant network by signing up high-end restaurants, hotels, and retailers.

Although the period saw fierce competition in the nascent credit card industry, Amex carved out a lucrative niche with an upmarket, service-oriented strategy. As we're going to be discussing in-depth shortly, this continues to be an incredibly durable competitive advantage.

In 1975, the company launched what would become one of the most iconic advertising campaigns in history: “Don't Leave Home Without It.” Created by advertising legend David Ogilvy, the campaign originally promoted the travelers' cheques, but eventually expanded to its cards as well. The slogan caught on instantly, and before long, it was part of the popular lexicon.

In 1977, James D. Robinson III became CEO and injected American Express with an ambitious vision for the 1980s. Robinson believed Amex could leverage its brand and customer base to build a financial services empire, creating a one-stop shop for banking, investments, insurance, besides just payment services. This ambitious strategy led American Express far beyond its card and travel core and would bring with it mixed results.

In 1981, the company made a high-profile acquisition of Shearson Loeb Rhoades, a Wall Street brokerage and investment bank, giving it a major presence on Wall Street. Two years later, it added Lehman Brothers to that portfolio (merging it into Shearson), followed in rapid succession with the addition of a large insurance provider and a financial advisory unit.

Simultaneously, Amex doubled down on the core card business, introduced new tiers, such as the Platinum Card in 1984. Initially, it was launched as invitation-only, offering higher service levels and perks, boosting the premium image around the brand.

Following this, the company released the Optima Card in 1987, which was its first true credit card (allowing revolving balances), enabling it to compete in the fast-growing consumer credit segment. By the end of the 1980s, the campaign slogan “Membership Has Its Privileges” perfectly captured the essence of American Express' strategy.

However, the aggressive expansion was starting to attract criticism and growing pains. Shearson Investment Bank struggled with trading losses and integration issues, and analysts debated that Amex's business segments lacked synergy. Many argued that the company's push into investment banking was undervaluing the core franchise, and by the early 1990s, the pressure to refocus was mounting.

In 1993, under the leadership of newly appointed CEO Harvey Golub, it began divesting all of its investment banking businesses, including the firm that would be on everyone's lips in the late 2000s.

From then on, American Express concentrated on its core businesses: charge and credit cards, travel services, and its existing international financial operations. In other words, the broad financial enterprise was dismantled and reshaped around what the company knew best. Amex expanded global card acceptance, forged international banking partnerships, and built its rewards program into one of its most valuable assets.

The Membership Rewards program was built on the already established Membership Miles. If you've ever used a credit card, you're probably familiar with the basic idea: cardholders earn points for spending money, which can be redeemed for things like flights, hotels, gift cards, and much more.

In the late 1990s, Amex also introduced its most legendary product: the Centurion Card (also known as the Black Card). The story of how it came to be is a perfect example of how a well-established company like Amex can manage to keep its finger on the pulse.

Rumors had circulated for years about an invitation-only card for ultra-high-net-worth individuals. The so-called “Black Card” was shrouded in mystery, whispered to carry eye-watering annual fees and unrivaled concierge services. Rather than dismissing the chatter, American Express embraced the idea, and in 1999, it launched the Centurion Card.

The product is still offered today, with American Express hand-picking eligible recipients based on their spending history. Membership begins with a $10,000 initiation fee and a $5,000 annual fee. Benefits include complimentary elite status with major airlines and hotel groups, access to virtually every airport lounge in the world, VIP treatment at hotels, 24/7 dedicated concierge service, and exclusive event access.

Yet beyond these perks, it provides something less tangible but equally valuable: prestige.

The new millennium brought fresh trials and transformations for American Express. In 2001, Kenneth Chenault took over as CEO, beginning a tenure that would last nearly two decades and be shaped by major external challenges and Amex's responses to them. Only eight months into his term, the 9/11 terror attacks shook American Express to its core. Its headquarters in Lower Manhattan was damaged in the collapse of the towers, and the company tragically lost 11 employees who were working in the World Trade Center that day.

While sharing in the shock and grief felt across the country and the world, American Express also had to adapt. Travel, a key revenue driver, came to a sudden halt in the aftermath of the attacks. Chenault steered the firm through the immediate crisis by supporting affected employees and customers while preparing the company for a difficult economic period.

In the years that followed, Amex regained its footing as travel rebounded and consumer spending returned, continuing to build its brand and expand its card business. But in 2008, the company confronted a true existential threat in the global financial crisis. With credit markets frozen and consumer spending collapsing, Amex needed a safe harbor. In November 2008, it made the strategic decision to convert into a bank holding company – a move that allowed it to accept deposits and qualify for federal support programs that ensured its survival.

The relationship between Buffett and American Express also deepened during moments of crisis. Berkshire Hathaway had begun accumulating shares during the 1990s, and during the 2008 financial meltdown, Amex faced severe liquidity pressures as credit markets froze. Berkshire backed the company with a $3 billion preferred share investment, providing vital capital at a moment when funding was scarce. Just as he had reasoned in 1963, the short-term turmoil mattered less than enduring trust in the brand.

Ultimately, American Express survived 2008, though not unscathed. Credit losses were heavy, and like many other financial companies, it had to cut costs through layoffs. But unlike some of the largest institutions, it avoided a full-scale government rescue, relying only on temporary funding programs. By 2010, it had repaid all federal aid and returned to profitability.

During the 2000s, the company also found itself navigating a changing competitive and regulatory landscape. A long-running legal battle over Visa and MasterCard's exclusionary rules (which had barred banks from issuing Amex cards) was resolved in Amex's favor in 2004, opening the door for American Express to partner with banks. The company promptly struck deals with MBNA and Citibank to issue American Express-branded cards.

Another dramatic competitive shakeup came from another iconic American institution: Costco. American Express had long been the exclusive credit card accepted at the retail chain through a co-branded card partnership. But in 2015, Costco ended the deal in favor of Visa. Losing Costco's high-spending customer base and transaction volume was a tough setback.

The company moved swiftly to offset the loss by doubling down on other co-brand deals and ramping up marketing to attract a broader range of customers. Additionally, Amex accelerated international expansion and invested heavily in digital capabilities such as mobile apps and contactless payments. By 2017, long-serving CEO Chenault could close out his tenure with American Express firmly back on a growth path.

By the 2020s, American Express had become a global payments network, operating in more than 100 countries and processing trillions in annual charge volume. Stephen J. Squeri, now a 40-year veteran of Amex, took over as Chairman and CEO in 2018 and has focused on a strategy of leaning into a digital transformation, while never losing sight of what makes it so special: its premium service. That has meant major investments in technology alongside a continued focus on delivering best-in-class customer service and offerings.

The pandemic dealt a sudden blow to one of the cornerstones of Amex's business as global travel ground to a halt. To keep cardmembers engaged, the company quickly pivoted its rewards toward everyday categories like groceries and streaming services. By 2021, as vaccines rolled out and travel resumed, spending on Amex cards rebounded sharply. Pent-up demand for leisure and travel fueled record volumes in several quarters, with premium products like the Platinum Card leading the surge.

“As we were going through COVID, it looked like we were going to lose money. And my decision was to invest more because my view was if we lose $5 or we lose $6, who gives a s***. It doesn't really matter, we're losing money, right? And the reality was, as long as your capital position, liquidity position is right, why not invest in your cardholders. We did that. We didn't lose any money. Wound up making money, didn't make as much as we had plan to make, but it kept the fuel in the tank. So then when we came out of COVID, we came out like a rocket ship as opposed to limping out.”

– Stephen J. Squeri, Chairman & CEO of American Express, at the Bernstein 41st Annual Strategic Decisions Conference 2025 (sourced through Quartr Pro).

That same straightforward style comes through in how he frames Amex's mission:

“[American Express] is not in the credit card business. We're in the relationship business.”

Let's take a closer look at how the relationship business translates into Amex's model and network.

Before diving into the details, it's important to understand that American Express operates an integrated payments model, distinct from Visa and MasterCard. Those networks run on an open-loop system, collecting fees on each transaction while banks issue the cards and capture interest and fees.

American Express operates a “closed-loop” system, serving as both the card issuer and the network. In practice, this means Amex not only provides cards directly to consumers and businesses but also signs up merchants to accept them. This structure gives the company end-to-end control over the relationship between cardmembers and merchants. By doing so, American Express captures value from both sides: merchant fees on transactions and interest and fees from cardholders.

The model also provides a data advantage. Acting as both issuer and network, Amex sees spending behavior on the customer side and acceptance patterns on the merchant side, giving it a more complete view than most banks get when issuing on Visa or Mastercard rails. This richer dataset allows Amex to analyze spending patterns, tailor offers, and manage risk more effectively.

The challenge with this model is that American Express must build its own merchant network rather than rely on an existing global one. That process has historically been slower, leading to an acceptance gap. Yet once a merchant joins the network and customers create an Amex account, the relationship tends to be highly sticky and lucrative. Over time, this dynamic has allowed the company to close much of the acceptance gap in its core U.S. market, with progress continuing internationally.

American Express' business model revolves around spending. Unlike most card issuers that rely primarily on lending and interest income (a “credit-centric” approach), Amex runs a “spend-centric” model. The company earns the bulk of its revenues when cardmembers use their cards. This works because Amex deliberately targets customers who tend to do two things: spend heavily and pay reliably. Time has proven this to be a winning formula.

In Q2 2025, American Express generated $63.4 billion in trailing twelve-month (TTM) revenue (net of interest expense and provisions). Roughly 80% came from fees tied to spending, while about 20% came from net interest income on cardmember loans. This mix reflects Amex's integrated, closed-loop network, which allows it to capture value at multiple points in each transaction.

Every time a cardmember makes a purchase, the merchant pays Amex a fee for processing that transaction. Known as the merchant discount rate (or “swipe fee”), this is Amex's single largest revenue source. In Q2 2025, merchant discount revenue totaled $36 billion on a TTM basis, comprising nearly 70% of fee revenue and more than 50% of the total revenue.

Amex has historically charged higher merchant fees than Visa, Mastercard, and Discover, which for years limited acceptance. But the company has steadily closed that gap by showing merchants the higher spending power its cardmembers bring. As highlighted during the Investor Day 2024, the average U.S. consumer spend per Amex card was three times higher than the average Visa or Mastercard credit card spend.

“What really powers the closed-loop network is the premium customer base. And when you look at our customers, 55% of our U.S. card customers make over $200,000 a year. Those are customers that our merchants want to connect to.”

– Stephen J. Squeri, Chairman & CEO of American Express, at the Bernstein 41st Annual Strategic Decision Conference 2025 (sourced through Quartr Pro).

Today, Amex has largely closed the acceptance gap domestically, with over 99% of U.S. merchants accepting its cards by 2024. The merchant fee itself varies by industry, merchant size, and other factors, but in recent years has averaged around 2.3% of transaction value. Those pennies on each dollar add up quickly with Amex's annual billed business reaching $1.6 trillion in Q2 2025 (TTM). Looking ahead, international acceptance remains the growth lever:

"By 2026, we aspire to reach 90 million total international accepting locations, achieve our initial goal of 75% coverage across all 48 priority cities and increase the number of countries with more than 75% coverage. We anticipate that achieving these aspirations by 2026 will significantly increase total international spend."

– Raymond Joabar, President of Global Merchant & Network Services of American Express, at its Investor Day 2024.

Another source of fee revenue comes from annual membership fees that come with many of its cards, especially its premium products. These net card fees totaled $9.2 billion in Q2 2025 (TTM), representing roughly 13% of total revenues and growing 19% year-over-year. Although there are numerous free alternatives available on the market, Amex has been successful in convincing customers to pay for membership by delivering rich rewards and exclusive perks. From 2019 to 2025, the share of fee-based vs non-fee-based has increased from 60% to 70%. During this same period, total cards-in-force grew from 114 to 149 million.

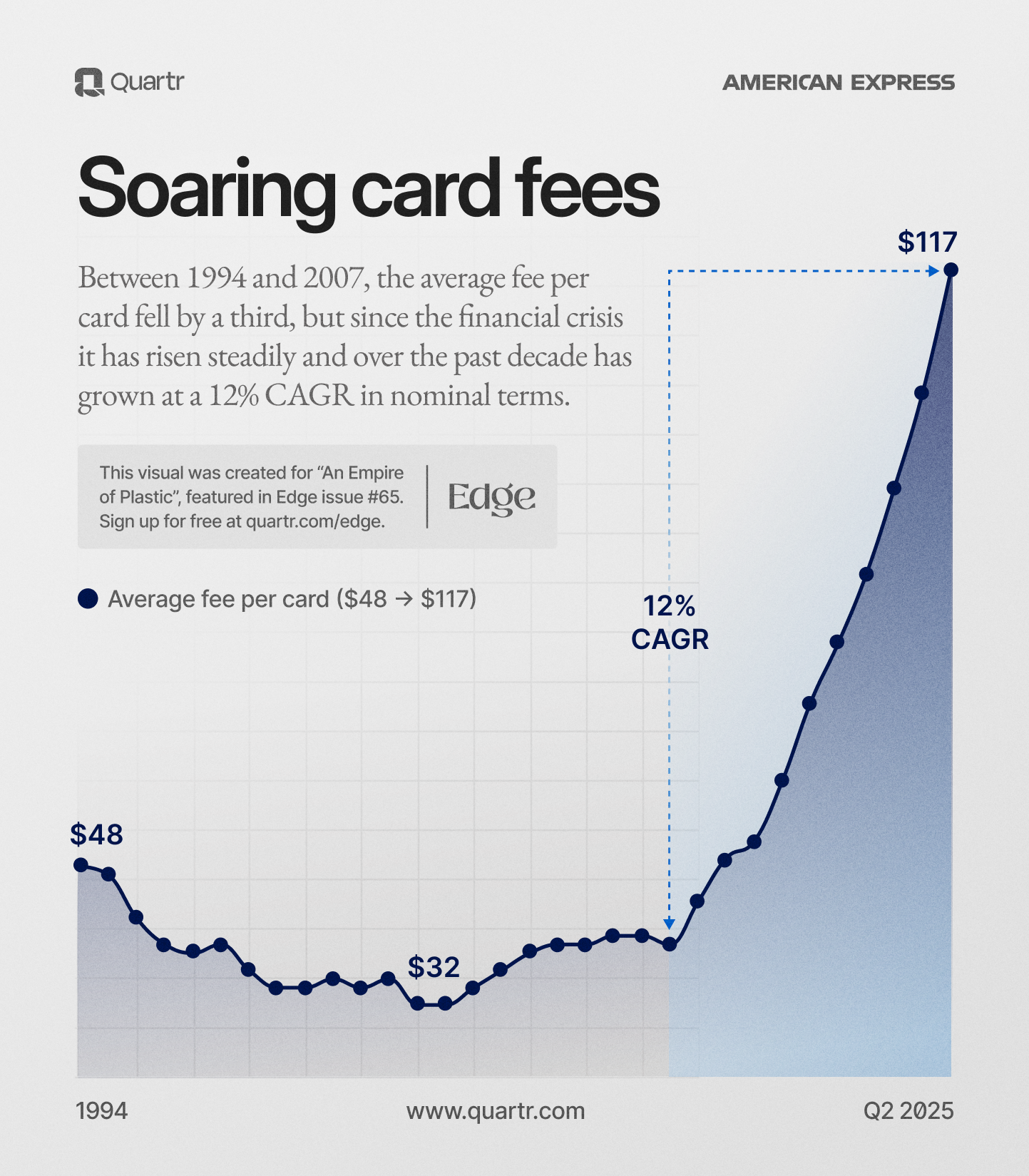

Crucially, this growth hasn't come from lowering fees. As the visualization below shows, the average annual fee per card has risen sharply in recent years, even as total cards-in-force and the share of fee-based accounts have increased.

The external comparison adds to the point: at the Investor Day 2024, the company highlighted that the average Amex card carries five times higher annual subscription-like fees than competitors. Taken together, American Express has managed to expand its customer base, grow the proportion of fee-based cards, and raise average fees.

American Express has managed this seemingly contradictory outcome, higher fees alongside strong account growth, through what it calls its Product Refresh Strategy. Amex systematically reworks major products every three to four years by first adding meaningful value and only then raising fees.

In practice, the company aims to deliver at least twice as much new value as the fee increase, often by co-creating benefits with partners who help fund them. The Platinum Card's 2021 refresh, for example, raised the annual fee by $145 but added more than $1,500 worth of credits and perks, while the 2024 Gold Card refresh boosted the fee by $75 yet delivered over $400 in additional value.

This partner-funded model has become a flywheel: brands like Delta Air Lines, Uber, Disney, and Saks tap into Amex's affluent customer base, subsidizing benefits that make its cards more compelling. The strategy's success shows in the numbers, with refreshed products driving double-digit account growth, near-99% retention, and still, with a rising average fee per account.

Beyond fees tied to spending and membership, Amex also runs a significant lending business, generating net interest income from balances carried by cardmembers. In Q2 2025 (TTM), net interest income was $16.4 billion, amounting to 20% of total revenue. That share has doubled since before the pandemic, driven by higher interest rates and growth in revolving balances. Finally, Amex earns revenue from a variety of smaller streams, including foreign exchange fees, delinquency charges, travel commissions, partner service fees, and network licensing.

All of the value added to membership comes at a cost. In Q2 2025 (TTM), American Express spent $22.7 billion on cardmember services and rewards, with rewards making up the majority. The growing stream of subscription-like revenues helps sustain these outlays. All in all, the trends outlined above have translated into exceptional profitability, with return on equity consistently in the low-30% range – among the highest in global finance.

Apart from its brand, a high-spending customer base is one of the company's greatest strengths and is in itself one of its strongest competitive advantages. As stated, American Express customers tend to spend significantly more than the average credit card holder and have excellent credit profiles. This higher spending per customer means more fee revenue per account, while the strong credit quality leads to lower credit losses.

When American Express discusses its customers, it refers to them as “Card Members” and presents it as a membership model with leading value propositions. Through its loyalty points program and the various perks, Amex incentivizes members to use their cards, as the more they spend, the more points they earn.

As previously mentioned, cardholders can also take part in exclusive benefits like airport lounge access, annual travel credits, concierge services, ticket presales for entertainment events, and various insurance protections. These features (which tend to accompany the higher annual fee cards in particular) create high switching costs for customers, as once embedded in the Amex ecosystem with accumulated rewards and accustomed to premium perks, it becomes difficult for customers to walk away.

“Our commitment to listening to our customers and doubling down on enhancing the value of American Express membership is what's driving our momentum.”

– Stephen J. Squeri, Chairman & CEO of American Express, at its Investor Day 2024 (sourced through Quartr Pro).

The model also generates powerful network effects. The more cardmembers Amex attracts (particularly high spenders) the more compelling it becomes for merchants to accept the card, making them willing to pay higher fees to reach these customers. In turn, the broader the merchant network and the richer the offers, the more attractive it is for consumers to carry and use Amex cards.

American Express' growth continues to come from the same engines that have long defined its model: attracting new customers, driving higher spending, and keeping cardmembers engaged. As we've already seen, spending, total cards-in-force, and membership fees have all climbed meaningfully in recent years. Underpinning that momentum is the company's refresh strategy of systematically adding value before raising fees, which has allowed Amex to expand both usage and loyalty at the same time.

A key driver of that momentum is the success Amex has had with younger generations, which, according to the company, are more accustomed to subscription-style models. Millennials and Gen Z have become a central focus of its strategy, representing over 60% of new consumer acquisitions globally and more than 75% of new Gold and Platinum accounts. For Amex, the opportunity lies not just in bringing them on board, but in showing that higher fees are justified when the value is clear.

“[Gen-Zs and millennials] are very value conscious, and they look at this, and they basically say, 'Look, for whatever the fee may be, I'm getting the value.' And if they don't feel they get the value from the Platinum Card, they can look at the Gold Card, and they get that. So I think it's good for the industry. I think pricing power is much more tied to the value you provide.”

– Stephen J. Squeri, Chairman & CEO of American Express, at its Q2 2025 earnings call (sourced through Quartr Pro).

Another area where Amex continues to push for expansion is its merchant network. While U.S. acceptance is now virtually on par with competitors, international growth remains a priority. Lower-fee programs for small businesses have added millions of new merchants, and strategic partnerships with local banks and payment aggregators have helped unlock markets.

In Australia, Amex has achieved near parity acceptance through partnerships with major banks, while in India, cards that once had limited use are now widely accepted online and at upscale retailers. Each new point of acceptance represents incremental spending that might otherwise have flowed to a competitor.

Of course, a spend-centric model ties Amex closely to consumer confidence. In strong economies, volumes rise quickly, amplified by the fact that its cardmembers disproportionately spend on discretionary categories that grow fastest in good times. In downturns, spending naturally slows and credit losses increase.

However, Amex is better insulated than most competitors thanks to its affluent customer base. Even in recessions, these cardmembers typically have the financial flexibility to maintain spending, softening the impact of economic swings that hit mass-market issuers much harder. Beyond the short term, the overall credit card industry continues to grow steadily year after year, providing Amex with a durable long-term tailwind.

American Express' most obvious competitors are Visa and MasterCard, which together dominate the global card payment ecosystem. While these companies don't issue cards themselves, their networks power the vast majority of credit and debit cards worldwide. They have acceptance virtually everywhere and benefit from an open-loop model where any bank can issue their cards, resulting in billions of their cards across all segments, from basic debit cards to high-end credit.

American Express competes with them on multiple fronts. For premium customers, Amex faces off against Visa Infinite and MasterCard World Elite cards issued by banks; products that try to match Amex's perks and often undercut on fees. Having an open-loop network is a clear advantage for these because consumers might choose a Visa Signature card simply because they know for sure it will be accepted even at that small bakery in the French countryside. American Express' response has been to go all-in on its superior service and rewards to justify choosing an Amex.

On the issuing side, major banks such as JPMorgan Chase, Citigroup, and Capital One are Amex's most direct rivals. They market credit cards to the same affluent customer base Amex targets, often relying on large sign-up bonuses, high cashback rates, or partner tie-ins to attract customers. Many of these products also carry lower annual fees and, by running on the Visa or Mastercard networks, offer the reassurance of near-universal acceptance – a combination that can make them compelling alternatives to Amex.

American Express competes by offering a full membership experience and not just a credit line, but that requires constant attention. At times, 'reward wars' have forced issuers to escalate points or cash back, pressuring Amex to respond. Partnerships add another layer of risk: when major partners change course, as Costco did about a decade ago, Amex can lose a meaningful share of customers in a short period. That's why it's important for Amex to keep co-brand relationships mutually beneficial.

Beyond these differently structured competitors, Discover (acquired by Capital One in 2025) has been a smaller-scale competitor with a similar closed-loop model. Its products traditionally appealed to the mass market, with no-annual-fee cards and high cashback on rotating categories, but limited international acceptance kept it from posing a real threat to Amex's premium niche.

By acquiring Discover, Capital One signaled that it too sees strategic value in uniting an issuer with an in-house network. We will see in the coming years whether the merged CapOne-Discover platform can evolve into a stronger competitor by combining its closed-loop network with a more spend-centric strategy.

In recent years, a new type of competitor has emerged in the form of fintechs offering alternative payment models, particularly Buy Now, Pay Later (BNPL). These services let consumers split purchases into interest-free installments, while providers earn their revenue from merchant fees.

The BNPL trend poses an obvious threat to Amex and credit cards at large, diverting online purchase volume that would otherwise go on a credit card. According to a Morning Consult survey in 2024, over 12% of Americans had outstanding BNPL loans, and 56% of U.S. consumers had tried some form of BNPL financing. The appeal is obvious: quick approval, no interest (if paid on time), and a controlled installment plan. For someone averse to revolving credit card debt, paying in 4 equal installments via Klarna can be a far more appealing option.

American Express has responded with Plan It, its BNPL feature that lets cardholders split large purchases into fixed monthly installments for a set fee without interest. This effectively mimics the BNPL value proposition while keeping the customer within the Amex ecosystem.

In summary, American Express' competitive landscape is multifaceted. The company's answer has been to lean harder into what makes it unique, while adapting where it adds value. And in a market large enough to support multiple players, Amex only needs to capture a large enough share of affluent customers to thrive.

Above all, what sets American Express apart is its brand. Carefully built and maintained since the 1800s, it remains one of the company's greatest assets and consistently ranks among the most valuable and trusted brands in the world.

Trust is one dimension of that brand, reinforced by Amex's reputation for customer service and protection. A fraudulent charge, a service not delivered, a cancelled flight? Amex will step in, refund the customer, and handle the frustrating process of recovery. This reliability has long made Amex the preferred choice for business travelers and consumers making large purchases.

Beyond trust, American Express has carefully cultivated an image of prestige. Its cards are symbols of status, marketed as membership in an exclusive club. The psychological appeal of being an Amex customer and holding a product tied to success adds an intangible but potent advantage that competitors can't replicate. The strength of the brand translates into remarkable loyalty. But don't just take it from us. This is how CEO Squeri put it:

"Many of our customers don't see themselves as simply having or using American Express cards. They feel they are with American Express. They have an emotional connection to our brand and the products and services we offer. Our card members are proud of their association with us. I often have people tell me how long they've been a member when I first meet them."

– Stephen J. Squeri, Chairman & CEO of American Express, at its Investor Day 2022 (sourced through Quartr Pro).

We began this article talking about Warren Buffett, and we're going to let him be the one to conclude it as well. While much can, has, and will be said about American Express, he perfectly summarizes it when he calls it a one-of-a-kind business. We'll leave you with these words of his:

You can't create another American Express.— Warren Buffett

Explore our platforms

Leading companies and financial institutions worldwide rely on Quartr to make better decisions faster.

Desktop

API

)

)

)